Latest Market Trading News

2nd July 2026

Andy Burnham and the threat of a bank tax raid.

With the resignation of Sir Keir Starmer on the 22nd of June 2026, political momentum has shifted towards Andy Burnham who is planning to take over the Labour party leadership and become prime minister. News has emerged that bankers and trade unions are bracing for a clash over a potential “tax raid” on UK banks to fund public infrastructure and housing.

A rapid “tax raid” on banks can reduce short-term business profitability, but investing on infrastructure and regional devolution can boost long-term economic growth (which supports a currency). The GBP will likely depreciate in relation to the US dollar or euro if foreign investors withdraw their money from UK financial institutions.

This could have a major impact on the shares of critical UK lenders such as Lloyds and Barclays which have faced downwards pressure from investors as they price in stricter regulatory costs and higher taxes on profits.

20th June 2026

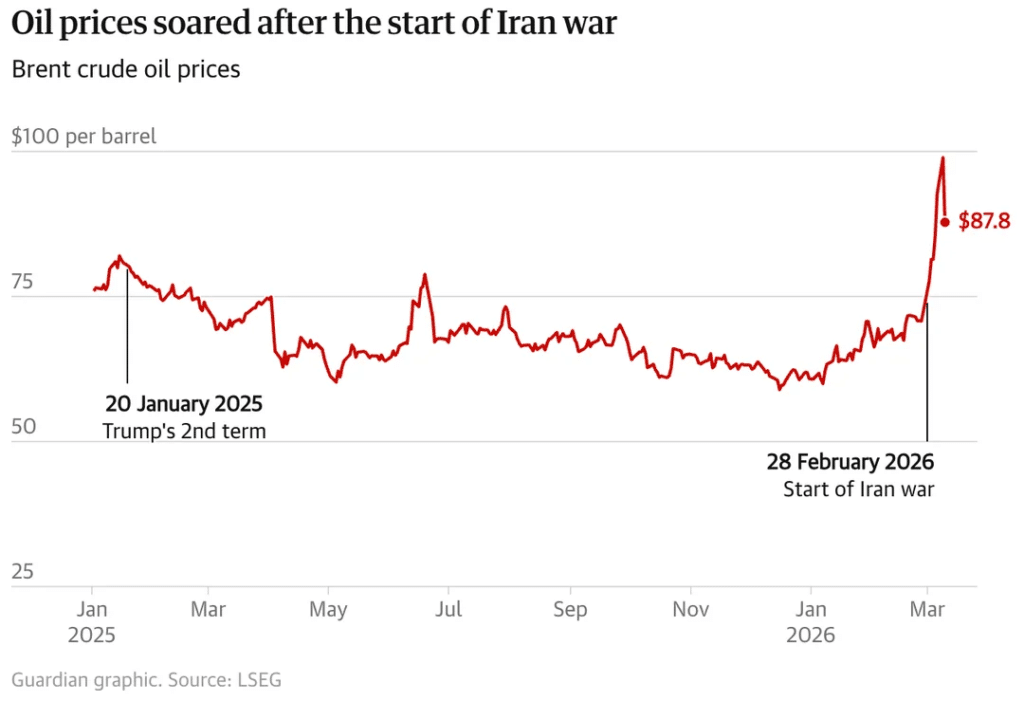

Impact of closure of the Strait of Hormuz on FOREX markets, CFDs and oil prices.

The impact of the closure of the Strait of Hormuz has triggered a sharp ‘risk off’ environment which has caused large scale capital flight (The rapid and large-scale exodus of financial assets and money from a country) into safer considered currencies such as the US Dollar (USD) as well as Japanese Yen (JPY) and the Swiss franc (CHF). This is because these countries are not considered to rely heavily on imported goods (in this case oil) and so are expected to remain stable in times of high volatility. Surging costs of crude oil and LNG prices influence import dependent countries which caused several ‘sell offs’ in these currencies especially GDP and EUR as illustrated in the diagrams below.

The effect on CFDs (contracts for difference) certainly did not go unnoticed either, with extreme market volatility, driving huge price spikes in energy CFDs with CFDs like (Brent and WTI crude surging past $90–$100+/bbl). This is explained by the simple concept of supply and demand. The Strait of Hormuz closes, a bottleneck of roughly 20 million barrels per day occurs. This reduces the supply of oil in the economy. As oil is a necessity for modern global transportation fuels and essential petrochemical materials, the good is in constant high demand. In response to this loss of supply in the economy the price of oil inflates rapidly leading to a bidding war amongst individuals and corporations for a limited stock. This is reflected by the sharp price spike shown in the flowing diagram.

14th June 2026

Changes to ER and the effect on FOREX markets

Following a softer-than-expected June Non-Farm Payrolls (NFP) report last week, which initially cooled assertive Fed hike bets, the dollar kept the upper hand. Traders are moving carefully and holding onto the USD ahead of the highly anticipated FOMC Meeting Minutes, as several Fed officials have maintained a hawkish underlying tone.

The Euro remains under pressure, struggling to find a clear level above the 1.1400 mark due to regional inflation concerns and a wider change into safe-haven assets. Conversely, the British Pound (GBP) has shown a strong rebound, supported by domestic stability and policy expectations from the UK’s incoming political leadership.

The Japanese Yen continues to trade near national and historic lows (toying with the 161–162 range against the dollar). While the wide US-Japan interest rate differential applies pressure firmly on the Yen, aggressive short-selling is being checked by heavy speculation that Japanese authorities may deploy unannounced, targeted interventions to punish speculators.

10th June 2026

Middle East Tensions Explode as Markets Brace for Uncertainty

Tuesday saw a sharp escalation in the conflict between the US, Israel, and Iran, making peace even more elusive. After accusing Iran of shooting down an American military helicopter close to Oman, President Donald Trump pledged to get revenge. Despite the fact that both pilots were saved, Washington quickly launched a new round of airstrikes against Iranian sites.

The devastation caused by the war is still ongoing. Over 7,000 people are said to have died in Iran and Lebanon, while fourteen American soldiers have been killed. Iran’s foreign minister, meanwhile, issued a strong warning, stating that foreign military forces operating close to Iranian land are still always in danger.

Financial markets are also being shaken by the global unrest. The durability of the AI-driven boom is being questioned as investors are withdrawing their funds from large technology stocks. Analysts caution that as global volatility continues to rise, an over-reliance on a small number of IT firms may leave markets vulnerable.

Investors may experience a wave of risk aversion if the conflict worsens, which may raise oil prices, increase demand for safe-haven assets like gold and the US dollar, and raise volatility in international equities markets.

27th April 2026

Global markets ready for testing

The three pillars of geopolitics, central banks, and tech profits will put global markets to the test this week. Stalled US-Iran discussions are impeding flows through the Strait of Hormuz and driving up oil prices, which is prompting increased fears about inflation and stagflation risk. The Middle East crisis continues to be the primary macro driver.

The second important axis is rates. The Fed is generally anticipated to remain stable, but messaging is crucial: Treasury rates are rising in reaction to inflation persistence and energy shocks, which lessen the likelihood of short-term reduction. Similar restrictions on central banks around the world (ECB, BoE, and BoJ) support a “higher-for-longer” policy.

Growth signals are still brittle. PMIs indicate a subtrend expansion with growing stagflation risks, while US manufacturing is weak and German mood remains low.

Earnings, particularly in AI-driven technology, are the final micro-level pillar that supports stocks.

Long energy/commodities bias, cautious stocks, a high volatility regime, and tactical USD/yield sensitivity are the positioning takeaways.

7th April 2026

Stress continues to dent risk appetite

Concerns over wider ramifications for equities indices are being raised as stress is starting to appear in a number of areas of the world’s markets.

Blue Owl Capital’s stock, which is frequently used as a gauge for the $1.8 trillion private credit sector, recently hit a record low after the company restricted withdrawals from two of its funds due to an increase in withdrawal requests. The action has heightened concerns about private credit’s liquidity risks, especially in light of the industry’s exposure to susceptible tech firms that could be disrupted by artificial intelligence.

Additionally, markets have experienced increased volatility due to geopolitical tensions associated with the intensifying war between the United States and Iran. Risk sentiment has been impacted by rising oil prices and the anxiety around a possible military escalation.

Major benchmarks have already shown the outcome. The Nasdaq 100 and the S&P 500 both fell by almost 5% in March, while bond markets also saw a dip as investors lowered their expectations that the Federal Reserve would slash interest rates.

The pressure on global equity indexes may worsen in the coming months if private credit stress increases or geopolitical risks worsen.

RISK OFF Atmosphere

26th March 2026

The start of the week has seen a distinct risk-off atmosphere in the financial markets, but with an odd configuration. Gold and silver are continuing their decline, while stocks are generally down. Concurrently, the rates on U.S. Treasury bonds are rising, indicating that investors are selling government bonds instead of finding refuge in them.

The oil shock associated with rising tensions in the Middle East, which has driven crude prices considerably higher and rekindled concerns about global inflation, is one of the main forces motivating these actions. Bond yields are rising and the US currency is gaining as a result of markets being forced to reprice interest-rate expectations due to rising energy prices. Because rising real yields make non-yielding assets like gold and silver less appealing, precious metals are under pressure in this climate.

Since investors frequently liquidate attractive holdings to cover losses elsewhere during times of market stress, a portion of the decline in metals may also be due to liquidity-driven selling.

Looking forward, a number of significant macroeconomic developments, such as flash PMI data, U.S. productivity statistics, the Richmond Fed Manufacturing Index, U.K. inflation data, and the University of Michigan consumer mood survey, might influence market sentiment this week.

The trajectory of U.S. rates is expected to continue to be the primary driver of global markets in the days ahead, with inflation and energy once again at the heart of the story.

19th March 2026

FOMC Meeting

Financial markets broadly anticipated the Federal Open Market Committee’s (FOMC) decision to maintain the federal funds target range at 3.50%–3.75% during its March meeting.

The Federal Reserve noted in its announcement that although inflation has decreased from its high, there is still uneven progress toward the 2% target. Policymakers stressed that future decisions will still rely on new information and that economic uncertainty is still high.

Jerome Powell was circumspect throughout the press conference. He reaffirmed that recent changes in energy costs and international tensions may make the disinflation process more difficult and that inflation, especially in the services sector, is still sticky.

The Fed is not rushing into rate decreases, which was a clear message for markets. Powell emphasized that before loosening policy, officials want more assurance that inflation is steadily approaching the objective. Because of this, expectations for short-term cutbacks might stay low, supporting the idea that U.S. monetary policy should be “higher for longer.”

9th March 2026

Oil surges

The largest bond market in the world is under pressure as rising oil prices send shockwaves across the world’s financial markets.

Crude prices have drastically increased, rekindling concerns about inflation as geopolitical tensions in the Middle East and threats around the Strait of Hormuz deepen. Oil is a vital component of the world economy, and when energy costs rise, so do the expenses of industry, transportation, and food.

The bond market has already responded. Investor predictions that inflation would stay high and that the Federal Reserve might have less leeway to lower interest rates caused the yield on the U.S. 10-year Treasury to rise to about 4.1%.

Because the U.S. Treasury market is the foundation of the global financial system, rising yields are important. Increased borrowing rates have an impact on government finance, corporate debt, and mortgages.

Equities, credit markets, and highly leveraged industries may become more susceptible to another wave of financial stress if energy costs keep rising and inflation pressures intensify.

The Fear Trade

4th March 2026

Financial markets have started to reflect growing global concerns. Equity futures have significantly declined and the US 10-year The dollar is strengthening, Treasury yields are rising, and oil prices are skyrocketing, with WTI trading close to $76 and Brent getting close to $83. This activity is not only indicative of a “risk-off” response. Rather, it seems that investors may be also accounting for the possibility of an inflation shock brought on by war.

The effects might go well beyond the financial markets if the dispute continues. Energy prices, transportation expenses, supply chains, and business profits could all probably be affected by the shock, which would eventually lead to increased inflation and pressure on household purchasing power.

In order to preserve liquidity and stabilize bond markets, central banks and fiscal authorities may need to step in. However, such actions would probably entail additional debt growth and financial assistance. These measures run the danger of increasing inflationary pressures on the actual economy, even though they might assist avoid chaotic market situations.

23rd February 2026

Light Opening Declines

Monday saw a decline in European stocks as risk appetite was affected by new uncertainty around U.S. trade penalties. Under pressure from an uncertain policy environment, the FTSE 100 nudged down 0.1%, the CAC 40 lost 0.2%, and the DAX plummeted 0.6% at the opening. The U.S. Supreme Court ruled that the emergency law did not permit the majority of last year’s tariffs, which caused markets to spike higher late Friday. But in response, Donald Trump announced a worldwide tax over the weekend that would be in effect for up to five months while the government looks for a more long-term legal solution. The tax would initially be 10% and subsequently 15%. Christine Lagarde, president of the European Central Bank, cautioned that commerce and investment are disrupted by the continuously changing “rules of the road.”

Europe’s STOXX 600 recently reached a new high, bolstered by strong earnings and strengthening data, despite Monday’s decline. The PMI data for the Eurozone also showed a positive surprise, with manufacturing once again reaching expansion territory. Nvidia’s results on Wednesday are the main event on the corporate calendar, but Europe has a busy earnings week. Ahead of a possible fresh round of nuclear negotiations between the United States and Iran in Geneva, oil prices also fell, with Brent trading close to $70.39 and WTI at $65.55.

16th February 2026

Expect risk-on/risk-off fluctuations throughout this choppy, holiday-shaped week.

A number of markets, including those in the United States, Canada, and several regions of Asia, are closed on Monday, which results in reduced liquidity and often “erratic” price movement in commodities and foreign exchange.

– On Tuesday, the 17th, momentum is bolstered by early U.S. activity readings (Empire/NAHB), Canada’s CPI, and UK labor statistics. On surprises, the GBP and CAD might move sharply.

– A significant U.S. “macro + Fed” block (housing/industry, FOMC minutes) and UK inflation are due on Wednesday, the 18th. Pay attention to the USD and rates’ response (2Y/10Y). Thursday 19: Housing and trade statistics between the US and Canada—helpful in fine-tuning the growth picture.

– Flash PMIs (U.S., Europe, and Japan), U.S. GDP (Q4), and, most importantly, Core PCE (the Fed’s preferred inflation measure) are the big events on Friday, the 20th. There will probably be volatility in gold and stocks.

2nd February 2026

Silver & Gold

After last week’s rally, gold and silver abruptly fell off. Gold, which had touched a record around $5,595 an ounce on Thursday, dropped back toward $4,700, marking one of the strongest pullbacks in decades. Double-digit intraday drops in silver caused margin calls and forced liquidation, making the impact even more severe.

The combination is well-known: higher rates, a stronger currency, and profit-taking on a crowded market, all of which have an adverse effect for non-yielding assets. Higher margin requirements on some metals contracts and predictions of a more hawkish Federal Reserve following Kevin Warsh’s nomination as chair contributed to the shock.

In summary, a quick leverage flush. Volatility could continue to be quite high in the short term; in the medium term, this appears to be more of a technical correction than a long-term trend reversal.

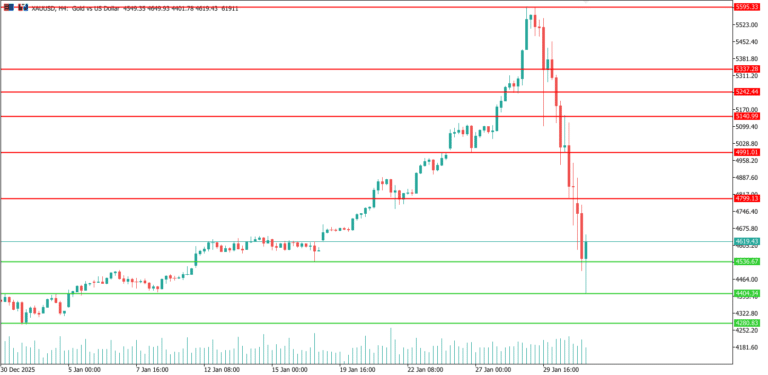

GOLD H4 chart

29th January 2026

FED decision on rates

The Federal Reserve paused three straight rate reduction on Wednesday, January 28, 2026, and maintained its benchmark rate in the range of 3.5% to 3.75%. The FOMC stated in its statement that the economy is still growing at a “solid pace,” that job growth is still moderate, and that the unemployment rate is beginning to stabilize. But inflation is still “somewhat elevated,” which encourages caution.

While maintaining the possibility of revisions in the event of unexpected new information, Jerome Powell stressed that the decision represented widespread agreement. In order to convey a less nervous tone, the Fed also eliminated any mention of increased employment risks.

As investors now focus on labor-market and inflation data ahead of the next meeting, markets, which had mostly priced in the hold, just slightly responded.

The Santa Claus Rally

15th Dec 2025

2nd Oct 2025

US Shutdown : Market uncertainty begins

US Shutdown : Market uncertainty begins

The shutdown of the US government is now a reality. Beyond politics, the Labor Department issues a pause—just when the economy is cooling down—the true market risk is a data blackout.

Background macro: Consumer confidence dropped to 94.2 from the predicted 96. At 3.2%, the hiring rate dropped to its lowest level since June 2024. There are somewhat more jobless people than available positions for a second month.

Market analysis:

Equities: Vulnerable, particularly those with significant multiple growth.

Treasuries: Long yields may decline due to flight to quality.

Dollar: Mixed (political noise against risk-off support).

Gold: Gains from reduced real rates and uncertainty.

How it could play out :

– Brief shutdown (≤2 weeks): As data resumes, there is a rise in volatility followed by a relief bounce.

– Layoffs plus prolonged shutdown(>2–3 weeks): Deeper decline, broader credit spreads, EPS downgrades, and higher claims.

Markets and investors fear uncertainty more than actual bad news, expect increased market volatility. US Indices have already began to breath, paring some of the recent gains.

Unmatched spreads.

11th Sep 2025

CPI Boss Fight: Will the Fed Swing 25 or 50?

The market is fighting for control when the August CPI is released on Thursday. The two things that seem exciting about a Fed cut next Wednesday are the amount and the rhetoric. The Fed may still cut 25 basis points if the CPI runs hot, particularly in core services (shelter, transportation, medical; ex-energy services), but it will be more tough about what comes next. However, a cold print would intensify rumors of a 50 bps move.

Core: 3.1% y/y (0.3% m/m), headline 2.9% y/y (0.3% m/m), according to consensus. Composition is the trapdoor. From February to May, core services averaged 0.2% m/m (~2.4% annualized); a 0.3% increase in August would raise the 3-month annualized pace to over 3.6%, which would feed concerns about “sticky inflation.” Indeed, companies are absorbing a portion of the tariff charge, lowering the prices of some commodities, and the PPI was unexpectedly lower. Wage pressure, however, is found in services inflation, which is also where the CPI index has significant weight.

Because of this, stocks feel both justified and jittery at record highs. Bulls claim that a weaker PPI combined with worsening labor data means that easing is likely. Bears counter: reducing sticky services could lead to stagflation. A hotter core is likely to rocket front-end yields, knock richly priced growth, and give the dollar a knee-jerk bounce (which some strategists would fade on labor concerns). Rate-sensitives and long duration are the pivot.

While gold hovers around records on cut hopes and oil slid as U.S. inventories built—an economic cool-breeze tale that markets prefer to hear before CPI—futures are green entering the print, aided by AI tailwinds (Oracle just staged a historic pop). As inflation turns out to be a little firmer than anticipated, the European Central Bank (ECB) is projected to hold, with both hawks and doves bolstering their cases but likely providing tight guidance.

Trader’s perspective (not advice): • Hot core (≥0.3–0.4% m/m): Front-end yields ↑; 2025 cut route reduced; gold softens; risk-off wobble.

• Cool core (≤0.2% m/m): higher yields, risk-on, bigger-cut buzz, gold steady/up, and dollar easing.

• Mixed: The Fed’s statement becomes the market’s metronome; composition comes before the headline.

In summary, the mix is more important than the level. Even if the initial cut comes on time next week, the glide path to easier policy becomes more difficult if that engine picks up speed again. Keep an eye on key services.

27th August 2025

Wall Street is mesmerized by Nvidia, yet risks lurk in the background.

The market’s fixation on one firm is overshadowing much larger threats that are simmering beneath the surface as Wall Street waits for Nvidia’s earnings.

Nvidia is now more than just a stock to investors; it’s a gauge of the mood of the market. The chipmaker is now carrying the burden of an entire rally after reaching previously unheard-of heights on the artificial intelligence boom. Analysts and traders alike are keeping an eye on Nvidia to see if it can produce strong margins, rapid revenue growth, and evidence that the demand for AI-powered processors is still unquenchable on a global scale.

The stakes are high: a beat might rekindle the exuberant momentum that has kept Wall Street afloat for months, while a failure on earnings or guidance could send shockwaves through equities. To put it briefly, Nvidia controls the market’s sentiment in addition to releasing financial data.

However, a political tempest is brewing in Washington as Wall Street is enthralled by a single ticker sign. The independence of the U.S. central bank is being called into question by former President Donald Trump’s attempt to oust Federal Reserve Governor Lisa Cook. Although the markets haven’t moved much, undermining the Fed could have significant effects on long-term interest rates, inflation, and the dollar.

Main Street, meanwhile, is raising its own warnings. With more Americans reporting that finding a job is becoming more difficult and inflation forecasts gradually rising, the Conference Board’s consumer confidence index fell in August. The forecast for the upcoming six months dropped to its lowest point in years, indicating that people are becoming increasingly concerned about the direction of the economy.

Nvidia’s story may have enthralled Wall Street, but investors who overlook the political and economic undertones run the danger of being caught off guard. Sometimes, the shadows—rather than the spotlight—present the true threat.

30 June 2025

Important Economic Events to Keep an Eye on This Week for Active Investors

There are a number of important macroeconomic events this week that might have a big impact on market sentiment and policy expectations. It will be essential for active investors to stay informed.

Germany’s preliminary June CPI data, a crucial determinant of the ECB’s inflation outlook, is released on Monday. Additionally, the UK will release its Q1 national accounts, which will include capital flows from the banking sector and data on corporate investments.

China, the Eurozone, the United Kingdom, and the United States will all release manufacturing PMI data on Tuesday. Given that growth forecasts are still shaky, these indicators will provide important information about the state of the global industrial economy.

South Korea’s inflation figures and Eurozone unemployment data will be the main topics of discussion on Wednesday. A number of mid-sized businesses in the luxury and retail industries in Europe will release their earnings, giving an indication of consumer demand following the second quarter.

Perhaps the most significant day of the week is Thursday. The focus will be on the US non-farm payrolls report (NFP). Expectations for the Fed’s next actions, and consequently the US currency and Treasury yields, could be directly impacted by any shocks in job creation, wage growth, or unemployment. Investors will also look for clues about upcoming rate decisions in the minutes of the ECB’s most recent meeting. Furthermore, considering the prominence of the service sector in developed economies, global services PMI numbers are due.

Last but not least, Friday will be calmer because of the US Independence Day vacation, which usually lowers liquidity in international markets and could increase volatility elsewhere. However, further information about the state of the European economy will be provided by Germany’s industrial orders as well as EU housing and PPI data.

In summary, traders are facing a high-stakes week as central bank narratives, employment, and inflation all play a role.

23 June 2025

As tensions in the Middle East worsen, oil prices rise, and markets are on edge.

Following recent U.S. airstrikes on Iran, which caused a dramatic increase in oil prices and heightened concerns about a bigger geopolitical crisis, global markets are on high alert. Oil futures have already jumped above $100, and some analysts have warned that prices might reach $130 or higher per barrel if the Strait of Hormuz is closed.

The Strait of Hormuz is one of the world’s most strategically important shipping lanes, handling around 20% of the world’s oil traffic. Any disturbance would cause shockwaves in the energy markets, raise the price of gasoline globally, and further strain already precarious global supply systems.

The stock markets are responding cautiously. Gold continues to be a reliable conventional safe haven during times of international unrest, while stock indices are declining as investors avoid risk. There are indications of technical weakness in the SP500, which could pave the way for another adjustment. In the meantime, institutional purchasing is fueling a spectacular bullish breakthrough in the oil markets. Although gold and bitcoin are still consolidating, they may rise quickly if tensions keep rising.

Additionally, the dispute poses a threat of expanding beyond the current U.S.-Iran conflict. Potential cyberattacks, sabotage, and economic reprisal are causes for increasing anxiety. Global powers like China and Russia may try to safeguard their interests, while regional players like Israel, Hezbollah, and the Houthis are keeping a careful eye on things. The deputy director of Russia’s Security Council, Dmitry Medvedev, made a bold statement after the U.S. strikes, saying that “several countries are ready to directly supply Iran with their own nuclear warheads.” Russia has sent a strong message to Washington by formally denouncing the assaults as a flagrant breach of international law and pledging its support for Iran.

Markets might collapse rapidly if Iran turns from threats to action. Investors and traders should prepare for high volatility.

19 June 2025

The Regional Conflict Between Israel and Iran Could Upend World Markets

The Israeli-Iranian confrontation is much more than a regional geopolitical quarrel. If the situation worsens, a complicated network of economic concerns might jeopardize the stability of the world economy.

Nearly 20% of the world’s oil supply passes through the Strait of Hormuz, a tiny passageway at the center of this threat. Even a little interruption may cause oil prices to rise sharply, possibly pushing crude well above $120 or even $150 per barrel. After years of ultra-loose monetary policy, central banks are already having difficulty stabilizing prices, and this energy shock would swiftly translate into a fresh inflationary surge.

Central banks like the Federal Reserve would be faced with a difficult choice in such a situation: either maintain high interest rates to fight inflation and run the risk of a catastrophic recession, or restore huge liquidity to the economy at the expense of undermining confidence in fiat currencies.

There would probably be a period of intense volatility in the financial markets. Investors would rush into hard assets like gold, silver, commodities, and strategic real estate, while major stock indices might see severe corrections.

This kind of crisis, however, has the potential to quicken a current trend: de-dollarization. Yuan or euros are already being used to settle some energy contracts. The U.S. dollar’s long-standing dominance would be called into question by a protracted crisis of confidence, which would have significant repercussions for the global monetary system.

The systemic risks are real, but full-scale escalation is still preventable. A regional war can swiftly turn into a worldwide financial shock in the connected world of today.

5 June 2025

ECB Goes Loose as Global Trade Remains Uncertain

Accommodative stance – The ECB’s eighth consecutive interest rate cut, down to 2%, signals an aggressive push to boost the bloc’s economy amid lingering fallout from Trump’s trade war. With inflation now below the ECB’s 2% target and core component showing signs of softening, the central bank is acting to ensure monetary conditions remain supportive. The cut had been anticipated by markets, but it underscores a broader shift toward policy easing as the ECB contends with external pressures, particularly from deteriorating global trade conditions and slower growth. Investors responded to the downward revision for 2026 growth with modest optimism and confidence that the ECB will remain accommodative. Expectations are now forming around a potential pause in July, and markets are likely to remain sensitive to future data releases, particularly if inflation pressures unexpectedly resurface or Trump’s trade rhetoric escalates further.

Jobs catalyst – U.S. stock indices edge higher as investors await the key non-farm payrolls report, in order to assess how Donald Trump’s trade policies are impacting the job market and the Federal Reserve’s interest rate outlook. While the central bank is expected to hold rates steady this month, markets are pricing in at least two cuts by year-end. Despite Trump’s repeated calls for lower rates, Fed Chair Jerome Powell remains cautious, preferring to wait for more economic clarity amid ongoing tariff uncertainty. Meanwhile, Washington’s tariffs on steel and aluminum have taken effect, with the threat of broader levies in July. Investors are now closely monitoring trade talks, particularly a potential call between Trump and China’s Xi Jinping.

Supply expansion – Oil prices declined amid growing signs that Saudi Arabia is pushing for another increase in output, reinforcing market concerns over a potential supply glut in the second half of the year. The proposed increase of at least 411,000 barrels per day underscores a strategic shift toward defending market share rather than prioritising price stability. This comes as the kingdom aims to capitalise on seasonal peak demand during summer months. However, such a move also heightens risks of oversupply, especially with inventories already showing signs of building and global demand forecasts remaining vulnerable to macroeconomic uncertainties. A more aggressive supply expansion may exacerbate downward pressure on prices. Compounding the bearish sentiment, Saudi Aramco’s price cut to Asia, though smaller than anticipated, signals weakening demand in key import markets.

22 May 2025

U.S. Fiscal Strains Boost Bitcoin At Expense of Commodities

New high – Bitcoin soared to a new all-time high above $111,000 on Thursday, extending its 2025 bull run even as U.S. equity markets pulled back. The world’s largest cryptocurrency continues to defy broader risk-off sentiment, driven by accelerating institutional inflows and growing regulatory clarity. Momentum has also been bolstered by progress on the regulatory front. The GENIUS Act – a bill designed to provide a framework for stablecoin regulation – cleared a key procedural hurdle in the U.S. Senate this week. Market participants and crypto advocates view it as a positive step toward removing uncertainty in the digital asset space. With regulatory tailwinds, strong inflows, and sustained institutional confidence, bitcoin’s rise is increasingly being seen not just as speculative mania, but as a maturing asset class solidifying its role in the financial system.

Output hike – Oil prices fell, pressured by expectations of increased output from major producers and rising concerns about global demand amid U.S. fiscal uncertainty. The sell-off was triggered by reports from Bloomberg that OPEC+ is considering a third consecutive production hike, with one proposal involving a July increase of 411,000 barrels per day – triple the group’s previously planned rise. The potential supply boost comes as oil markets already grapple with subdued demand signals, amplifying downside risks. In parallel, investors are growing uneasy over mounting U.S. debt. A tax-cut and spending bill through Congress have added to fears about fiscal sustainability, shaking broader market confidence. All eyes now turn to OPEC+’s June 1 meeting for clarity on the cartel’s next move.

Critical juncture – The U.S. House of Representatives passed a sweeping tax-and-spending bill by a single vote, enacting much of Donald Trump’s economic agenda while intensifying fears over the nation’s ballooning debt. The legislation is projected to add $3.8 trillion to the federal deficit over the next decade. Markets reacted with mixed signals. U.S. stock futures edged higher after the bill’s passage, but Treasury yields climbed, reflecting investor anxiety about government borrowing. Meanwhile, the U.S. dollar faced fresh selling pressure as global confidence in American fiscal discipline continues to erode, aggravated by Trump’s unpredictable tariff policy and mounting international skepticism toward the stability of U.S. assets. As political divisions deepen and long-term fiscal reform remains elusive, the market sees the U.S. finding itself at a critical juncture.

15 May 2025

Uncertainty Reigns as Geopolitical Talks Unfold

Renewed optimism – Bitcoin traded higher helped by renewed institutional flows back into US-listed spot bitcoin exchange-traded funds. The rebound in ETF activity came as inflation worries eased and trade tensions between the US and China showed signs of de-escalation. Lower-than-expected CPI helped bolster risk appetite and fuelled speculation that the Federal Reserve may be able to cut interest rates later this year. Despite the improved backdrop, market uncertainty, especially over global trade dynamics, continues to cap gains. Traders are expected to watch Friday’s producer price data and Fed commentary closely for further cues.

Fragile peace – Ukraine and Russia may hold long-awaited talks in Turkey today, but uncertainty shrouds the summit amid conflicting signals and a lack of high-level participation. Despite calling for the talks himself, Russian President Putin will not be attending. Ukrainian President Zelensky has said he will make a final decision on whether to attend after meeting with Turkish President Erdogan. US President Trump, who had signalled openness to adjusting his Middle East visit to join the summit, will also be absent. With global pressure mounting, both US and European leaders have warned that Moscow faces fresh sanctions if it fails to engage seriously and agree to a ceasefire.

Supply concern – Oil prices fell amid rising expectations of a US-Iran nuclear agreement that could lead to sanctions relief and increased Iranian oil exports. President Trump signalled that a deal was “very close,” with Tehran having “sort of” agreed to the terms. An Iranian official also indicated willingness to proceed in exchange for sanctions relief, following four rounds of talks in Oman. Despite this diplomatic progress, the US Treasury imposed new sanctions targeting Iran’s missile production and oil export networks, underscoring the fragile nature of the ongoing negotiations. Market sentiment was further pressured by a surprise rise in US crude inventories. The Energy Information Administration reported a build of 3.5 million barrels last week, contrary to analyst expectations for a 1.1 million-barrel draw, fuelling concerns of oversupply.

08 May 2025

Art of Deal Strikes Again

Suspense deal – Gold prices slipped as optimism over a potential US-UK trade deal weighed on safe-haven demand. The move followed Donald Trump’s announcement of an imminent agreement, with a press briefing scheduled for 2 p.m. GMT. The prospect of easing trade tensions has led investors to reduce gold exposure, favoring risk assets instead. Recent gains in gold, which recently hit record highs above $3,500/oz, have largely been fueled by geopolitical uncertainty and aggressive tariff rhetoric. However, the appetite for the metal appears to be softening as signs of diplomatic progress emerge. Meanwhile, a stronger US dollar added further pressure, making gold more expensive for non-dollar buyers. Market sentiment remains cautious, though. While investor interest in gold remains historically elevated, demand from the jewellery sector has faltered, limiting upward momentum. Looking ahead, traders will watch for confirmation of the US-UK deal and any developments in US-China negotiations. If diplomacy gains traction, gold may trend lower in the near term, while a breakdown could trigger another spike in safe-haven flows.

Timid recovery – Oil prices rebounded following US President Donald Trump’s announcement of a forthcoming trade deal—widely expected to be with the UK—boosting market sentiment amid lingering concerns over global demand. The move offers a political win for Trump ahead of crucial US-China trade talks and has helped lift crude off recent lows sparked by tariffs and OPEC+ supply adjustments. While oil has faced downward pressure in recent weeks due to fears of a global slowdown and increased output from OPEC+ members, the prospect of a new trade agreement and falling US crude inventories is offering some near-term support with stockpiles dropping by 2 million barrels last week, according to the Energy Information Administration, partially offsetting Tuesday’s bearish API report showing a 4.49 million barrel build.

01 May 2025

Risk Appetite Makes Return

Risk on – Gold prices continued their decline midweek as investors scaled back safe-haven exposure amid renewed signs of US-China trade engagement. The pullback marks gold’s third straight session of losses, driven by optimism that fresh talks could ease tariff tensions. Traders will be watching for confirmation of any formal dialogue between Washington and Beijing before the weekend. Furthermore, sentiment has been lifted by Trump’s executive orders easing auto tariff pressure and remarks pointing to possible deals with India, South Korea, and Japan. Looking ahead, with geopolitical risk premia unwinding and trade dialogue showing signs of progress, the precious metal may face further downside pressure near term. However, any breakdown in talks could quickly reverse the market mood.

Tech support – Stronger-than-expected Q1 results from Microsoft and Meta lifted sentiment across the tech sector, offsetting concerns about a potential advertising slowdown linked to tariff uncertainty. Microsoft delivered robust earnings, with EPS of $3.46 on $70B in revenue, surpassing forecasts. Notably, Azure revenue rose on the back of AI demand, slightly above expectations. Commercial cloud revenue saw continued enterprise demand despite macro headwinds. Meta also outperformed, posting EPS of $6.43 and $42.3B in revenue, well above estimates. Guidance for Q2 revenue came in strong at $42.5B–$45.5B, despite management acknowledging ongoing tariff-driven ad market concerns. The dual beats and solid outlooks from two Magnificent 7 heavyweights provided a tailwind for the Nasdaq index.

New deal – The newly signed US-Ukraine agreement granting Washington a share of profits from Ukraine’s future mineral and energy sales reflects a shift toward longer-term strategic and economic cooperation. While not a formal security guarantee, the deal gives the US tangible stakes in Ukraine’s post-war recovery and resource access, helping to justify continued US support amid political debates over aid. The deal may bolster sentiment in energy and mining equities tied to US interests, particularly those with exposure to lithium, rare earths, or natural gas. However, uncertainty around control of resource-rich territories and absence of binding security commitments could temper investor enthusiasm in the near term.

17 April 2025

Central Banks Go Dovish Over Clouded Economic Outlook

Grim outlook – Markets remain nervous as the U.S. central bank struck a cautious note about the growth outlook. Federal Reserve Chair Jerome Powell is caught between a rock and a hard place as tariffs are likely to stoke inflation. Speaking publicly for the first time since President Trump paused parts of his sweeping tariff plan, the Fed boss signalled a wait-and-see approach to interest rates, saying the Fed needs more clarity on the economy’s trajectory. However, he warned that the ongoing trade turmoil could derail the central bank’s inflation and employment goals. The uncertainty has bruised dollar-denominated assets across the board with the greenback slumping to a three-year low against a basket of major currencies. U.S. stocks and bonds also have seen sharp outflows in recent weeks.

Cloudy sky – The euro held steady as the ECB slashed interest rates by 25 basis points on Thursday, bringing its key deposit rate down to 2.25% as trade tensions rattle the eurozone’s economic outlook. The move, widely expected by markets, follows growing uncertainty tied to U.S.-led tariff hikes that have roiled global commerce. In a stark policy statement, the central bank flagged “rising trade tensions” as a key driver of deteriorating growth prospects, with President Christine Lagarde warning of “exceptional uncertainty” ahead. Europe now faces a sharp uptick in U.S. tariffs—climbing from 3% to roughly 13%—creating what Lagarde called a “negative demand shock.” While many tariffs have been paused, the lingering threat of escalation has cast a shadow over inflation expectations and economic momentum.

Mounting pressure – While the week wraps early for commodities ahead of Good Friday, bullish drivers have outweighed bearish signals. Crude prices are set to notch a weekly gain, buoyed by fresh U.S. sanctions on Chinese firms trading Iranian oil. The move adds to mounting pressure on Tehran and raises the prospect of tighter global supply, especially as the Trump administration intensifies efforts to curb Iran’s nuclear ambitions through economic means. The International Energy Agency also added upward momentum by trimming its forecast for global supply growth. In its latest monthly report, the agency cut its forecast for this year by 260,000 barrels per day, now expecting a rise of just 1.2 million bpd. The revision reflects weaker-than-anticipated output from the U.S. and Venezuela, adding to market concerns over tighter supplies amid rising geopolitical tensions.

10 April 2025

Mixed Trade Policy Keeps Investors on Edge

Tariff Reloaded – Markets staged a dramatic rebound at Thursday’s open after President Donald Trump made a surprise reversal on tariff policy, temporarily slashing new import duties to 10% for most U.S. trade partners over a 90-day period. The sharp pivot marked a stark contrast to his earlier hardline stance and triggered a powerful rally across Wall Street. The S&P 500 soared in its third-biggest one-day gain since World War II, the Dow posted its strongest advance since the COVID crash of March 2020, and the Nasdaq exploded in its second-best session ever. Despite the relief rally, trade tensions remain high. The reciprocal tariffs Trump had long threatened officially came into effect, targeting nearly 90 countries. China was notably excluded from the temporary reprieve, with tariffs on Chinese goods escalating sharply after Beijing announced fresh duties on U.S. imports. The European Union also hit back, approving its first wave of countermeasures in response to the earlier U.S. steel and aluminium tariffs, signalling that the global trade skirmish is far from over.

Empire Strikes Back – The escalating showdown has rattled all asset classes, stoking fears of a growth slowdown, rising inflation, and squeezed corporate earnings. Amid the mounting uncertainty, gold has seen a sharp rally, as investors seek safety in traditional havens. China has fired back once again at President Donald Trump’s escalating tariff offensive, announcing a steep increase in duties on U.S. imports. Starting April 10, tariffs on American goods entering China will soar to 84%, up from the previous 34%, according to the latest statement from the Office of the Tariff Commission. The move comes in direct response to Washington’s own overnight hike, which pushed tariffs on Chinese goods past the 100% mark. This tit-for-tat trade war is rapidly deepening, threatening to paralyse commerce between the world’s two largest economies.

OPEC Strains – Oil prices remain fragile even though OPEC’s production slipped in March, just ahead of a planned output increase, as key members faced disruptions and mounting geopolitical pressure. Nigeria scaled back deliveries to domestic refineries, notably the Dangote facility, leading to a decline that offset stronger export volumes. Meanwhile, renewed efforts by U.S. President Donald Trump to choke off oil flows from Iran and Venezuela contributed to further production drops from those nations. In total, output from Nigeria, Iran, and Venezuela each fell by around 50,000 barrels per day. Despite this, Nigeria remains slightly above its OPEC+ production target, with Gabon identified as the bloc’s least compliant member. The latest figures highlight the fragile balance within OPEC+ as it begins to cautiously unwind some of its recent cuts. The full impact of the planned production hike may ultimately hinge on the success of Washington’s push to curtail supplies from Tehran and Caracas.

07 April 2025

Markets in Turmoil Amid Escalating Trade War

Asian and European markets suffered a major blow as the fallout from President Donald Trump’s sweeping tariff announcements triggered a global sell-off. In Asia, Hong Kong’s Hang Seng Index experienced a historic crash, while Taiwan’s TAIEX tumbled to an all-time low in a dramatic market rout. The chaos spilled into Europe, where the UK’s FTSE 100 opened sharply lower and Germany’s DAX endured a full-blown bloodbath at the open. Although European markets have since clawed back some losses, volatility remains high as investors brace for more turbulence amid the escalating trade showdown.

US futures are pointing to a rough start on Wall Street, with the S&P 500 expected to open down, reflecting deepening investor unease. Meanwhile, Brent Crude prices have slumped to their lowest level since April 2021, underscoring growing concerns over global demand. Even cryptocurrencies, often touted as alternatives to traditional finance, have been swept up in the turmoil. In a sell-off as widespread and intense as this, few risk assets are managing to escape the fallout unscathed.

04 April 2025

Geopolitical and Trade Escalations Fuel Market Jitters

Military Standoff – The U.S. is stepping up its military presence in the Middle East, with Defense Secretary Pete Hegseth sending in extra warplanes for an ongoing bombing campaign in Yemen. The move adds more fuel to the fire in Washington’s standoff with Iran, as Trump continues to push for nuclear negotiations—using both tariffs and military threats as leverage. Over the weekend, Trump warned Tehran that more strikes (and even more tariffs) could be on the way if talks don’t move forward. Iran, however, isn’t budging. In a firm response via Oman, Tehran made it clear that it won’t negotiate under pressure. With both sides digging in, tensions remain sky-high. Unless some behind-the-scenes diplomacy works its magic, we could be looking at more economic and military maneuvers, which would keep markets—and the energy sector—on edge.

Trade Turmoil – Wednesday’s much-anticipated tariff announcement couldn’t come at a trickier time for the markets. Stocks have been on a rollercoaster ride for weeks, thanks to ever-changing trade policy chatter, and investors are still feeling pretty jittery. Unfortunately, it doesn’t look like this latest move will do much to calm nerves. In fact, things might get even messier—China, Japan, and South Korea are reportedly teaming up to hit back at Trump’s tariff push. A coordinated counterstrike from these economic heavyweights could mean an extended trade skirmish, potentially tangling up supply chains and putting a damper on global growth. As traders sift through the details of this two-step tariff plan, all eyes will be on possible exemptions and any hints of a diplomatic breakthrough. And let’s not forget the Fed—already juggling economic curveballs, officials may have yet another headache if rising import costs start stoking inflation concerns.

Oil Balancing – OPEC turned down the oil tap a little in March, trimming production by 110,000 barrels per day (bpd) as it tried to keep supply in check before ramping things up again in May. According to Bloomberg’s latest survey, the group’s total output now stands at 27.43 million bpd, with members being reminded to stick to their quotas. This cut is all part of OPEC’s ongoing effort to keep oil markets steady and prices supported, despite unpredictable demand. Meanwhile, OPEC+ is still set to move forward with its planned production hikes, adding 138,000 bpd in May after a similar bump in April. As usual, traders will be keeping a close eye on OPEC’s next moves, since oil price stability remains a delicate balancing act—especially with geopolitical uncertainty and shifting demand trends in the mix.

21 March 2025

Markets Move on After Dovish Fed Decision

Stay safe – The gold market remains in the upward direction, hovering near recent highs as the Federal Reserve maintains a neutral monetary policy stance—despite raising its inflation outlook and trimming its growth forecast. As widely expected, the Fed held interest rates steady within the 4.25% to 4.50% range. However, policymakers provided little forward guidance, leaving markets guessing about the timing of future rate moves. The updated dot plot projections remained unchanged from December, showing rates ending the year at 3.9%, with further declines to 3.4% in 2026 and 3.1% in 2027. While the central bank appears in no rush to cut rates, it is adopting a more measured approach toward its balance sheet—adding another layer of complexity to the market’s outlook.

Stake high – Geopolitical stakes remain high in Ukraine with renewed airstrikes escalating tensions and fueling market uncertainty. President Volodymyr Zelensky accused Russia of deliberately targeting civilian sites, including hospitals, while suggesting that Putin has effectively dismissed a comprehensive ceasefire. The renewed hostilities come after Putin’s recent conversation with former U.S. President Donald Trump, in which the Russian leader reportedly conditioned any ceasefire on the cessation of Western military aid to Ukraine. With no immediate resolution in sight, geopolitical uncertainty remains a key risk factor for global markets, potentially triggering further volatility in energy prices, equities, and safe-haven assets.

Caution ahead – The US dollar saw little bid after the Federal Reserve held interest rates steady and reaffirmed its projection for two rate cuts in 2024. While the central bank revised its economic outlook, some analysts interpreted the announcement as dovish, reinforcing expectations for eventual easing. Risk assets bounced back following the Fed’s commitment to rate cuts, with equities gaining traction as investor sentiment improved. However, the greenback faced renewed pressure, reflecting shifting rate expectations. The updated forecasts indicate that policymakers remain cautious, aiming to balance inflation risks with economic stability, leaving markets closely watching the timing of the first rate cut.

14 March 2025

Markets Choose Flight to Safety

Hold still – The British pound remains supported ahead of the Bank of England’s (BoE) Monetary Policy Committee (MPC) meeting on 20 March, where policymakers are widely expected to hold rates steady at 4.50%. The central bank had previously cut rates by 25 basis points in February, but rising geopolitical risks and tightening global financial conditions have reinforced expectations of a pause. The impact of US trade policies, particularly Trump’s tariff measures, has already pushed UK bond yields higher, contributing to a stronger pound. While domestic economic indicators remain mixed, the BoE appears reluctant to continue easing in an environment where external shocks could sustain inflationary pressures. Markets will be watching for any forward guidance that could shape expectations for the BoE’s next policy move, which is likely to influence sterling’s trajectory in the near term.

Hard hit – Global equities experienced a sharp sell-off this week as investors repriced risk in response to growing concerns over US economic stability. Even President Trump’s economic team has acknowledged potential turbulence ahead, a shift that has fuelled risk aversion across asset classes. The Dow Jones Industrial Average tumbled 4%, while the S&P 500 extended its recent losses. The Nasdaq Composite suffered the most significant decline, plunging 4.5%. The tech sector led the decline, with the “Magnificent Seven” stocks driving the sell-off. The pullback reflects broader macroeconomic uncertainty, compounded by Trump’s aggressive trade policies. The US-Mexico-Canada trade negotiations remain unresolved, keeping markets on edge as investors assess potential tariff impacts on corporate earnings and economic growth.

New high – Gold prices have staged a strong recovery, supported by renewed safe-haven demand amid ongoing market volatility and geopolitical risks. Despite a slight cooling in inflation pressures, the latest US CPI data failed to alleviate broader recession fears. The Consumer Price Index (CPI) rose 0.2% in February, below expectations of 0.3% and down from 0.5% in January. Although gold experienced a sharp decline at the end of February—dropping over $130 to touch $2,833—technical support at key moving averages provided a floor for prices, leading to a swift rebound above $2,900. This resilience suggests that bullish sentiment remains intact, with market participants continuing to hedge against economic uncertainty.

07 March 2025

Markets Retreat as Geopolitics Takes Over Monetary Policy

Rally on hold – Markets are on edge as investors weigh the fallout from Trump’s sweeping tariffs on major US trading partners. The new measures—25% tariffs on Canada and Mexico, along with a sharp increase in China duties to 20%—went into effect on Tuesday. Canada wasted no time hitting back with its own round of immediate tariffs on US imports, while China responded with a 15% levy on American farm products like chicken and pork, set to take effect on March 10. However, Beijing’s relatively measured response left some analysts speculating that there’s still room for negotiation with Washington. With trade tensions heating up, investors are bracing for potential market turbulence in the days ahead. The S&P 500 has tanked to its November lows just above the 5700 mark. Any major escalation in the trade spat could spark a deeper correction in the coming weeks.

Geopolitical chessboard – Gold prices are taking a breather as traders lock in some profits after a strong recovery earlier this week. The price action is seemingly trying to hold onto its bullish momentum. Fundamental-wise, safe-haven demand continues to underpin gold, fuelled by rising geopolitical tensions and a sharp decline in the U.S. dollar index this week. Adding to the global economic mix, China’s National People’s Congress kicked off its annual session by reaffirming its 5% growth target for 2025, most likely as a defiant signal to Mr Trump’s aggressive foreign policy. On the eastern front, Trump claimed that Ukrainian President Volodymyr Zelenskyy had expressed gratitude for U.S. support and signalled a willingness to sign a deal granting the U.S. access to Ukraine’s mineral rights. Mixed statements such as this add yet another layer of complexity to the ongoing geopolitical chess match.

Swift comeback – The euro flexed its muscles against most major currencies after the European Central Bank’s latest interest rate move. As expected, the central bank trimmed rates by 25 basis points. But what really caught the market’s attention was Christine Lagarde’s tone during the press conference. Rather than signaling a dovish pivot, the ECB president struck a more hawkish note, stressing that future rate cuts would depend on incoming data. That cautious stance gave the euro a solid lift, as traders recalibrated their expectations for her next moves. Adding fuel to the rally, the euro is also buoyed by optimism over Europe’s growth following Germany’s proposal for a massive €500 billion infrastructure fund. The plan is seen as a potential counterweight to global trade tensions, offering a boost to the region’s economic outlook. The bullish news compound the bearish sentiment on the U.S. dollar which stumbled across the board, dragged down by mounting concerns over the impact of tariffs on inflation and broader economic growth.

28 February 2025

Markets Jitters as Trump Goes Against Rest of the World

Cautious approach – Markets are gaining confidence as investors digest Nvidia’s strong earnings, which reassured them about AI growth despite initial concerns over DeepSeek and weakening demand. While the company’s profit outlook initially sparked some hesitation on Wall Street, Nvidia’s stock rebounded after an early dip. At the same time, traders are closely watching President Trump’s latest tariff threats, which have added to existing economic jitters. On Wednesday, he vowed to slap 25% tariffs on the European Union and reinstate paused duties on Canada and Mexico. However, the lack of clear details left markets guessing about the timeline and potential impact. The S&P 500 is trying to squeeze out modest gains the latest session, in an attempt to end its five-day streak of losses.

Bouncing back – The euro-dollar exchange rate has pulled back to its mid-February lows around 1.0400 as the US Dollar remains strong amid a risk-off mood. Still, caution might be warranted as the remarkable strength of the US dollar in recent months has been challenged by a string of underwhelming economic reports—ranging from a dip in consumer confidence to sluggish retail sales and weak consumer sentiment—has shaken markets and fuelled concerns about the strength of the U.S. economy. Investors are now weighing whether these signals point to a temporary slowdown or a more persistent challenge ahead. Nevertheless, the greenback could benefit from erratic tariff decisions by Donald Trump against European and Japanese imports, making it the least vulnerable of the majors out there.

Wild ride – Bitcoin’s wild ride in its 6-figure valuation took a sharp turn downward as the digital gold plunged to its lowest level since November, dragging the broader crypto market down with it and erasing nearly half a trillion dollars in value. After soaring past $108,000 last month—coinciding with Donald Trump’s inauguration and his self-proclaimed status as the “Bitcoin President”—BTC is struggling to stay above $85,000. The selloff has been partly linked to growing investor frustration over Trump’s unfulfilled promises nearly a month into his term, adding another layer of uncertainty to an already volatile market. On a more technical level, expiring bitcoin options sitting in crypto exchanges, worth an estimated $3.9 billion, could expire out of the money, as most positions were set at higher price levels, further exacerbating market volatility. The crypto market also took another hit after a massive hack on the Bybit platform, described as the “biggest digital heist ever.” Hackers managed to steal around $1.5 billion by gaining control of an Ethereum wallet on the Dubai-based exchange. The shock of the breach, combined with Bitcoin’s price collapse, has sent ripples through the industry, intensifying concerns over security vulnerabilities and regulatory scrutiny.

21 February 2025

Unfettered Risk Appetite Keeps Brewing

Safe bet – Sustained demand for gold keeps the chart trajectory upward as investors weigh monetary policy against geopolitical winds. Hawkish FOMC meeting minutes released on Wednesday reinforced market expectations that the Federal Reserve will keep rates on hold for an extended period. This could discourage traders from making new bets, creating a headwind for the non-yielding metal. However, a renewed decline in US Treasury bond yields is keeping dollar bulls on the back foot, providing further support for gold prices. More importantly, the broader fundamentals still favour an upward trend for bullion, keeping the metal’s two-month rally intact. Gold’s bullish momentum is fuelled by concerns that President Donald Trump’s trade tariffs could spark a global trade war, boosting demand for the safe-haven metal.

Tables turned – The S&P 500 is inching up in a timid manner as market participants fret that a peace talk between the US and Russia without Ukraine could signal a dramatic shift in US foreign policy. The tension between President Volodymyr Zelensky of Ukraine and President Donald Trump reached new heights after the latter took to social media to mock Zelensky, calling him a “dictator without elections.” Zelensky fired back, accusing Trump of falling for Russian disinformation regarding the war in Ukraine. The heated exchange followed a controversial meeting between American and Russian officials in Saudi Arabia to discuss ending the war—without Ukraine at the table. After the meeting, Trump suggested Ukraine had initiated the conflict, prompting a swift and sharp rebuttal from Zelensky. The rhetoric highlights the risk of the US pulling the plug on Kyiv’s war effort, alienating its European allies in the process.

Still hodling – Bitcoin continues to defy concerns from the Federal Reserve’s latest meeting minutes, which signalled officials remain hesitant to cut interest rates anytime soon. The Fed pointed to trade policies under the Trump administration as a potential obstacle to controlling inflation. Despite this cautious stance, Bitcoin continued its rally, holding steady as investors shrugged off rate uncertainty and focused on the broader bullish sentiment in the crypto market. Bitcoin’s price tends to move in tandem with interest rate expectations because lower rates mean more liquidity in the market, making speculative assets like cryptocurrencies. Added uncertainty from the Ukraine geopolitical twist might have convinced more investors to pour into the digital gold.

14 February 2025

Ukraine Optimism Offsets Trade Worries

Inflation still hot – The much-anticipated U.S. inflation figure came out hotter than expected, throwing a wrench into hopes for near-term rate cuts. January’s consumer price index (CPI) rose 3.0% year-over-year, slightly above the expected 2.9%. The “core” CPI, which strips out food and energy, came in even stronger at 3.3% versus the anticipated 3.1%—marking the hottest inflation reading in months. These numbers bolster the case for monetary policy hawks who argue the Federal Reserve should hold off on cutting rates. Fed Chair Jerome Powell testified before the House Financial Services Committee, reiterating that the central bank is in no rush to cut rates, prioritising the fight against inflation. However, President Trump took to social media, pushing back and insisting the U.S. needs lower interest rates. The U.S. dollar index initially spiked on the inflation report but later gave up gains to trade lower. Meanwhile, the 10-year Treasury yield climbed to around 4.65% following the data, keeping limited support to the greenback.

Stabilisation factor – The oil price slump gained momentum as President Donald Trump took his first major step toward brokering an end to Russia’s war in Ukraine, just weeks after his inauguration. Trump took to social media to announce that he and Russian President Vladimir Putin agreed to start negotiations immediately, adding that he would be calling Ukrainian President Volodymyr Zelenskiy to inform him of the conversation. A potential ceasefire could further weigh on oil prices if Trump pushes to roll back sanctions on Russia’s energy sector. On a more fundamental level, the market’s depressed sentiment has been fuelled by rising U.S. crude stockpiles and hawkish comments from Fed Chair Jerome Powell signalling that the Fed isn’t rushing to cut interest rates. Higher interest rates tend to slow economic activity and weaken oil demand.

Steady climb – Wall Street reacted to the latest American CPI data with a knee-jerk selloff, but S&P 500 has found support and is still consolidating near its recent highs. A key factor? Reports that President Trump had a “productive” phone call with Russian President Putin about ending the Russia-Ukraine war, offering investors a glimmer of optimism, which would offset concerns with rising global trade tension, notably with the new administration’s reciprocal tariffs. On the corporate side, the fourth-quarter earnings season rolls on. So far, more than 69% of S&P 500 companies have already released their results, and the majority are delivering pleasant surprises—over 75% have topped Wall Street’s forecasts, according to FactSet.

7 February 2025

Trade Spat Casts Shadow Over Sentiment

Record high – Gold prices surged to yet another all-time high in this week’s trading, driven by strong safe-haven demand as investors flock to the yellow metal amid rising uncertainty. Market nerves remain on edge as President Trump’s unpredictable and potentially disruptive policy moves keep traders guessing. Meanwhile, China-U.S. trade tensions are heating up, with both nations escalating tariffs and taking further hostile business actions against each other this week. The EU may not be spared either after Trump doubled down on his plan to hike tariffs on the block, adding another layer of uncertainty to global trade dynamics. Experts fret that this “elevated trade policy uncertainty” could drag on economic growth in the coming months, primarily by dampening business investment and weakening market confidence. Goldman Sachs has warned that the eurozone economy could suffer a “sizable hit to activity” from the rise in trade tensions. With geopolitical and economic uncertainty mounting, gold continues its record-breaking rally, proving once again that when uncertainty reigns, gold shines.

Mixed feelings – U.S. stocks have recouped their recent losses as they strive to hold onto this year’s limited gains. While earnings from Alphabet and AMD fell short of expectations, Big Tech found support thanks to a strong rally in Nvidia. Alphabet’s stock took a hit, sliding nearly 7%, after its fourth-quarter cloud revenue came in below estimates. The shortfall raised concerns that the company’s aggressive AI investments may take longer than expected to pay off. However, Nvidia emerged as a winner, climbing more than 5% as investors bet that the chipmaker could benefit from the ongoing AI spending spree. Overall, a retreat of the 10-year Treasury yield to its lowest level since December 2024 further added support to the market’s rebound.

Sluggish demand – Crude oil prices tumbled to their lowest levels of the year as fears of weakening demand rattled investors. The drop comes after China announced retaliatory tariffs on U.S. crude oil imports, while U.S. stockpiles climbed for the second straight week. WTI crude hit its lowest point since December 31, 2024, as tensions between the top two consumers escalated. With China—the world’s largest oil importer—facing economic headwinds, concerns are mounting over a potential slowdown in global energy demand. On Tuesday, China’s State Council Tariff Commission announced a 15% tariff on U.S. coal and liquefied natural gas (LNG), along with a 10% duty on American crude oil, farm equipment, and certain vehicles, set to take effect next week. Meanwhile, fresh data from the U.S. Energy Information Administration (EIA) showed a larger-than-expected rise in U.S. crude inventories, reinforcing fears of weakening demand and adding further pressure to oil markets.

31 January 2025

AI Race and Safe Haven in Tandem

Tech correction – US tech stocks stabilised after plunging on Monday due to the sudden rise of Chinese artificial intelligence (AI) app DeepSeek. The open source solution sent chipmaker Nvidia into a nosedive, triggering a broader selloff across the market. The turbulence followed DeepSeek’s claim that its AI model was developed at a fraction of the cost of its competitors, prompting investors to rapidly reassess their bets on AI and the ROI on the costly infrastructure, and casting uncertainty over America’s AI dominance. President Donald Trump called the moment “a wake-up call” for the US tech industry while downplaying concerns over the breakthrough, affirming that the US will remain a leading force in AI. For traders following the price action, unless the Nasdaq sinks below its 2-month lows around 20600 the index is merely consolidating near its historic high. The market’s eventual resilience would prove the optimism surrounding AI investments that has fuelled much of the US stock market’s surge over the past two years.

ECB easing – The European Central Bank (ECB) delivered its fifth rate cut on Thursday, trimming interest rates by 25 basis points as it walks a tightrope between rising inflation and sluggish growth. After months of cooling, inflation in the eurozone is heating up again, hitting 2.4% in December – its third straight increase – just as the effects of cheaper energy start to fade. At the same time, the region’s economy is stuck in neutral. Fresh data showed zero growth in the final quarter of 2024, falling short of economists’ modest 0.1% forecast and following a 0.4% expansion in the previous quarter. Commenting on the latest move, ECB President Christine Lagarde didn’t sugarcoat the situation, admitting that the euro area economy is “set to remain weak in the near term.” In other words, while inflation is picking up, growth is taking a nap – leaving the ECB with the tricky job of keeping both in check. FX-wise, the single currency is far from being out of the woods as the US Fed stayed put with its interest rates unchanged, broadening the differential between the two economic entities.

Shining again – Gold is back on its feet after dragging its feet for the past three months. The price has surged to a new all-time fuelled by strong safe-haven demand and technical buying. Investor jitters over the new US administration’s trade and foreign policies – especially the potential for fresh tariffs – are keeping the marketplace on edge. Meanwhile, the Federal Reserve wrapped up its FOMC meeting on Wednesday with a clear signal: interest rates are staying unchanged for the foreseeable future. Policymakers acknowledged that “inflation remains somewhat elevated,” but Chair Jerome Powell downplayed any shift in stance, brushing off the change in wording as mere “language clean-up.” Powell steered clear of commenting on how President Trump’s policies might influence the Fed’s decisions. Markets, in turn, took the Fed’s statement and Powell’s press conference in stride, showing little reaction.

24 January 2025

Trump 2.0 May Complicate Fed Policy Course

Technical recovery – The euro’s current rebound is likely to be due to profit-taking after it hit a 26-month low earlier this year. General sentiment remains downbeat as the ECB keeps pushing in the loosening direction while the Fed is taking their feet off the pedal. President Christine Lagarde and other senior officials expressed support for additional rate cuts, potentially weakening the shared currency in the short term. Markets have already priced in another 25bp cut next Thursday, the fifth of the easing cycle, with expectations that interest rates will drop to 2% by year-end. Adding insult to injury would be the looming U.S. tariffs championed by Trump 2.0 elevating the risk of higher inflation in a fragile economy. Despite Lagarde’s reassurance that the central bank is “not overly concerned” about external factors, the market always finds a way to play in a cynical and pragmatic way and may keep the lid on the exchange rate.

Verbal escalation – Gold is surfing on renewed geopolitical tensions following Mr Trump’s inauguration. Stakes in the eastern front have been raised as the new U.S. president looks to boast his ‘art of the deal’ by settling the war in Ukraine in a swift manner. He delivered on his own social media platform Truth Social this week an ultimatum to his Russian counterpart Vladimir Putin saying that Russia should strike a deal or face even tougher economic consequences. Warnings of extending sanctions on all Russian exports to the United States and secondary penalties for nations conducting business with Moscow may push the latter to a corner if a deal fails to materialise, exacerbating the divide between the East and the West. The precious metal’s solid run lately in spite of the dollar’s strength signals growing demand for its safe haven status.

Clash of the titans – The U.S. dollar has given back its recent gains as traders await a new catalyst from the central bank’s interest rate decision next week. To spice things up, Powell & Co’s cautious stance puts the Federal Reserve on a potential collision course with the new assertive president. Donald Trump has increased pressure on the Fed to lower borrowing costs in a significant manner. As far as the market is concerned, the Fed is expected to keep its benchmark rate steady at 4.25-4.5% next week, in the wake of three consecutive cuts since September. However, policymakers have adopted a more conservative approach for the year especially as Mr Trump’s plans to raise tariffs, cut taxes, and tighten immigration policies could complicate efforts to lower inflation to the 2% target.

10 January 2025

UK Worries Weigh on Cable

Mini crisis – The pound has plunged to its lowest level in over a year, while UK borrowing costs have reached a 16-year high. The latest bond market sell-off reflects investors’ growing concerns over UK assets and most importantly the contrasting signal between higher gilt yields and a falling currency shows investors’ doubt over the country’s economic outlook and the health of its public finances. The market turmoil has added pressure on Chancellor Rachel Reeves, who faces increasing scrutiny, made an uncommon move by issuing a public statement for the second consecutive night, emphasising her “iron grip” on public finances. But despite government efforts to stabilise the markets, borrowing costs continue to climb. Addressing an urgent question in the House of Commons, Treasury Minister Darren Jones assured there was “no need for an emergency intervention” in financial markets. However, market participants still have the memory of the mini-budget crisis under the former prime minister Liz Truss in September 2022.

Seasonal demand – Brent crude is staging a steady recovery to its 3-month high as the market demand has shifted its focus to colder weather than the last two winters, in both Europe and the United States, which could boost consumption of heating oil. A stronger U.S. dollar and an unexpected rise in U.S. stockpiles have not deterred buyers from shying away, with technical buying-the-dips compounding the seasonal factor. There are high hopes that the recent weak CPI print in China would spur more stimulus to tackle the country’s chronic economic headache. In the meantime, a surge in travel across China ahead of the Lunar New Year has improved demand expectations, adding to rationales that would help the price stabilise in the near term.

Bullish consolidation – The December U.S. jobs report was a blowout for the outgoing administration with the unemployment rate dropping to 4.1%. The print was a confirmation that would lessen the worry about the impact of high interest rates on the job market. While the market participants await further rejuvenation of the economy under Trump 2.0, the earnings season is kicking off next week with Q4 and full-year results from Wall Street’s big banks. Investors anticipate impressive numbers as trading volumes have significantly exceeded typical fourth-quarter levels across all asset classes, fuelled by a growing participation from retail traders amid a bull run in both stock and cryptocurrency markets.

3 January 2025

Investors Remain Confident about U.S. Growth

Parity in sight – The market is waiting for fresh catalysts in the first week of 2025 and the upcoming U.S. nonfarm payrolls might just give participants enough a reason to stay alert. A strong reading could be the straw that broke the euro’s back as the single currency is inching towards the parity threshold, last seen in November 2022. The market consensus is that Trump’s policies will sustain support for the greenback, as tax reliefs will put upward pressure on inflation and make further interest rate cuts less easy to justify, while tariffs against the eurozone would be seen as rubbing salt in the wound, undermining its growth outlook.

Steady recovery – Gold is striving for a comeback after it stabilised around its recent low of $2,600. The precious metal gains strength thanks to its safe-haven appeal, as investors turn their attention to President-elect Donald Trump’s upcoming administration, set to begin on January 20. Anticipated policies from Trump, including higher import tariffs and lower taxes, are expected to benefit gold. More specifically, elevated tariffs could spark a global trade war, while reduced taxes may increase inflationary pressures in the United States. Gold often thrives in times of economic uncertainty as a safer asset and performs well during periods of rising inflation, as investors use it to hedge against price increases. Meanwhile, 10-year US Treasury yields fall to approximately 4.5%, reducing the opportunity cost of holding non-yielding assets like gold, enhancing their attractiveness.